What to Review Before Taking Out Equity Release Mortgages

What to Review Before Taking Out Equity Release Mortgages

Blog Article

Checking Out the Various Kinds Of Equity Release Mortgages Available Today

Equity Release mortgages existing various options for home owners aged 55 and over. equity release mortgages. These financial products satisfy different requirements and preferences, enabling people to access funds from their residential or commercial property. From life time home mortgages to shared appreciation home mortgages, each kind supplies distinctive benefits. Recognizing these options is important for making educated decisions. What elements should one take into consideration when choosing one of the most suitable equity Release strategy? The details that adhere to may lose light on this crucial subject

Understanding Equity Release Mortgages

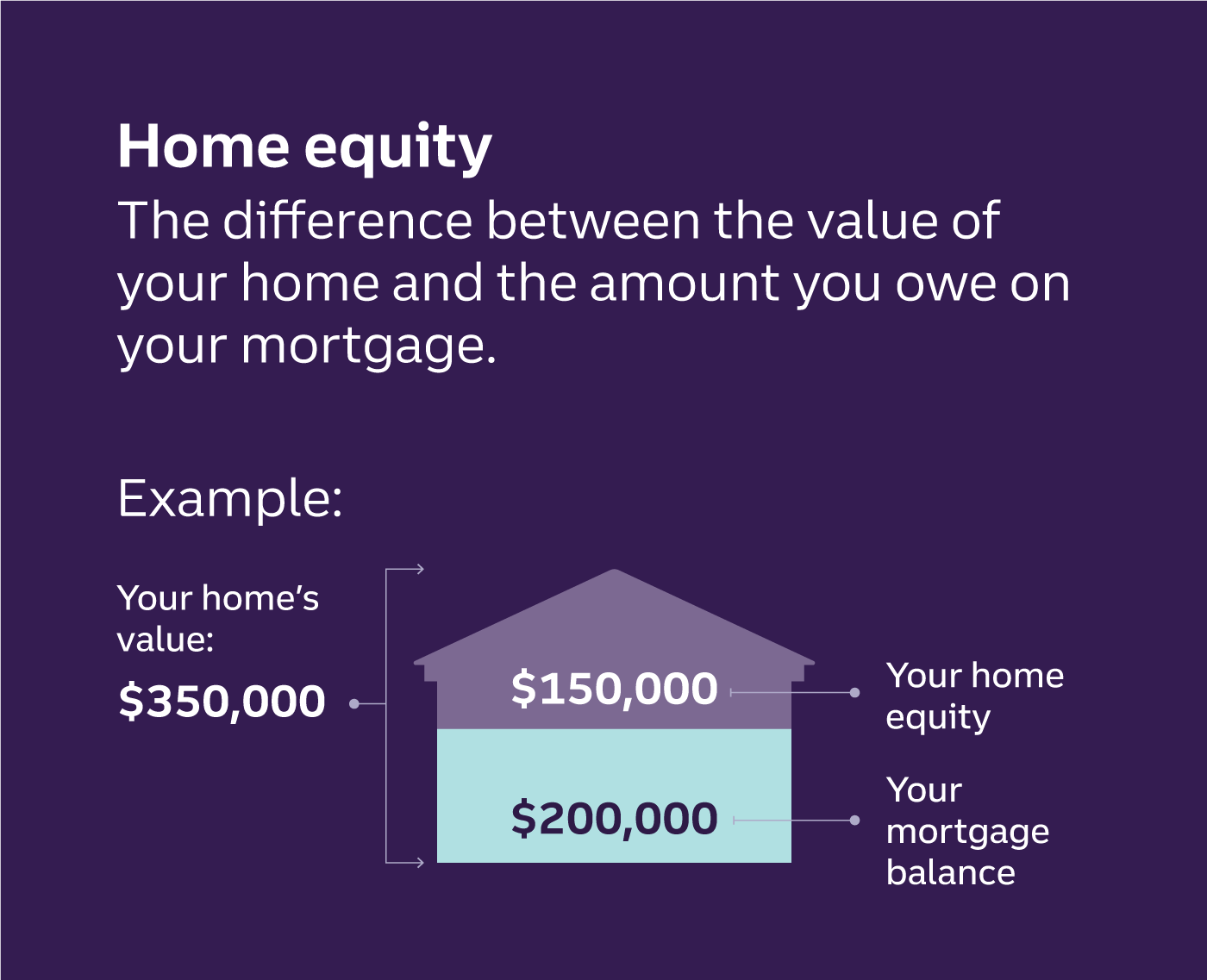

Equity Release home loans offer home owners, commonly those aged 55 and over, with a way to access the worth locked up in their property without needing to offer it. This economic choice allows people to convert a section of their home equity right into cash, which can be utilized for numerous purposes, such as home enhancements, settling financial obligations, or funding retirement.Equity Release can take different types, yet it essentially includes borrowing versus the value of the home while keeping possession. Home owners can select to get a lump amount or a collection of smaller payments, relying on their economic demands and preferences.Additionally, the quantity readily available for Release is affected by the residential property's worth, the home owner's age, and specific lending institution standards. Generally, understanding equity Release mortgages is vital for property owners to make educated decisions regarding tapping right into their home's equity while considering the long-lasting ramifications.

Life time Mortgages

Lifetime home loans stand for among the most prominent kinds of equity Release. This monetary product permits property owners, usually aged 55 or older, to borrow against the value of their property while preserving ownership. The lending, which is safeguarded versus the home, accumulates passion gradually but does not require regular monthly repayments. Instead, the loan and accrued interest are repaid when the home owner passes away or moves right into lasting care.Lifetime home loans provide flexibility, as debtors can pick to get a round figure or select a drawdown center, accessing funds as needed. Significantly, many plans featured a no-negative-equity assurance, guaranteeing that customers will certainly never owe greater than the value of their home. This attribute offers assurance, allowing people to enjoy their retired life without the concern of depleting their estate. On the whole, life time mortgages act as a feasible option for those looking for financial assistance in later life.

Home Reversion Plans

Drawdown Life Time Mortgages

While many house owners seek ways to access their wealth, drawdown lifetime home mortgages provide a flexible option that permits people to Release funds gradually. This kind of equity Release home loan allows homeowners to obtain against the value of their residential property while retaining possession. Unlike traditional lifetime mortgages, drawdown plans allow consumers to access a portion of their equity upfront and withdraw additional funds as needed, as much as a fixed limit.This function can be specifically beneficial for those who wish to manage their funds thoroughly, as it reduces rate of interest build-up by just charging interest on the amounts drawn. In addition, drawdown life time home mortgages frequently include a "no negative equity warranty," making certain that debtors will certainly never owe greater than their home's value. This choice suits retirees who prefer economic safety and security and adaptability, permitting them to satisfy unanticipated costs or maintain their lifestyle without needing to market their building.

Boosted Lifetime Mortgages

Improved Life time Mortgages supply unique advantages for eligible home owners seeking to Release equity from their homes. Recognizing the eligibility standards is necessary, as it identifies who can take advantage of these specialized loans. It is also important to assess the prospective downsides associated with enhanced choices, making certain an all-round point of view on their usage.

Eligibility Requirements Described

Recognizing the qualification standards for Improved Life time Mortgages is vital for possible candidates seeking to access the equity in their homes. Generally, applicants need to be aged 55 or older, as this age requirement is conventional in the equity Release market. Property owners must possess a home valued at a minimum limit, which can vary by lender. Notably, the home must be their key house and in excellent condition. Lenders often evaluate the property owner's health and wellness standing, as certain health and wellness problems might enhance qualification and benefits. Furthermore, applicants must not have existing considerable debts secured against the residential property. Meeting these requirements enables people to explore Improved Life time Home mortgages as a viable choice for accessing funds locked up in their homes.

Benefits of Improved Mortgages

After clarifying the eligibility criteria, it becomes noticeable that Boosted Life time Home mortgages use numerous substantial benefits for homeowners looking to utilize their building equity. Largely, they supply accessibility to a bigger financing amount compared to typical lifetime mortgages, benefiting those with health conditions or age-related factors that increase their life span threat. This improved borrowing capability allows home owners to fulfill various economic requirements, such as home enhancements or retired life costs. Furthermore, these home mortgages normally include versatile settlement choices, enabling debtors to manage their funds much more properly. The no-negative-equity guarantee even more assures that homeowners will certainly never owe more than their building's worth, supplying comfort. Generally, Boosted Lifetime Home mortgages present an engaging alternative for eligible home owners looking for monetary services.

Potential Downsides Considered

While Boosted Life time Home mortgages offer numerous benefits, prospective drawbacks call for cautious factor to consider. One substantial worry is the influence on inheritance; the equity released decreases the worth of the estate entrusted to recipients. In addition, these home loans can build up significant rate of interest with time, bring about a considerable debt that may surpass visit their website the initial loan quantity. There might additionally be restrictions on residential or commercial property alterations or rental, restricting house owners' flexibility. Enhanced products often require particular health and wellness problems, meaning not all homeowners will certainly qualify. Managing the fees and costs associated with these home loans can be complex, potentially leading to unexpected prices. Because of this, individuals must thoroughly examine their situation and consult monetary experts prior to proceeding.

Shared Recognition Mortgages

Shared Admiration Home loans stand for an unique economic plan that allows homeowners to gain access to equity while sharing future home worth boosts with the lender. This strategy provides potential benefits such as decreased month-to-month settlements, however it additionally features disadvantages that need to be thoroughly taken into consideration. Recognizing the eligibility needs is essential for those curious about this choice.

Concept Summary

Equity Release home mortgages, especially in the form of common recognition home loans, provide homeowners a distinct monetary option that permits them to gain access to funds by leveraging the worth of their property. In this arrangement, a lender supplies a lending to the home owner, which is generally paid off through a share of the residential or commercial property's future recognition in worth. This implies that when the home owner sells the home or passes away, the lending institution gets a percent of the boosted worth, as opposed to simply the preliminary loan amount. Shared gratitude home loans can be appealing for those looking to supplement their revenue or money significant costs while retaining possession of their home. Nevertheless, the economic effects of common admiration must be very carefully considered by possible customers.

Advantages and Drawbacks

Common gratitude home mortgages can provide significant monetary advantages, they likewise come with notable disadvantages that potential customers ought to consider. These home loans permit home owners to access equity in their properties while sharing a part of any type of future recognition with the lending institution. This arrangement can be useful during times of increasing residential property worths, providing substantial funds without regular monthly settlements. However, the primary downside is the potential loss of equity; homeowners may end up with considerably lowered inheritance for beneficiaries. Additionally, the complexity of the terms can result in misconceptions regarding payment obligations and the percentage of gratitude owed. It is necessary for customers to evaluate these factors carefully before committing to a shared appreciation home mortgage.

Eligibility Requirements

What requirements must home owners fulfill to receive a common admiration mortgage? Primarily, prospects should go to the very least 55 years of ages, ensuring they are within important site the target demographic for equity Release products. In addition, the building should be their main residence and normally valued above a specified minimum limit, frequently around ? 100,000. Lenders also examine the homeowner's economic conditions, including earnings and exceptional debts, to establish they can handle the home mortgage properly. Notably, the building should be in good problem and devoid of significant legal encumbrances. Home owners ought to additionally have a clear understanding of the terms, consisting of exactly how recognition will be shared with the lender upon sale or transfer of the residential property, as this influences general returns.

Selecting the Right Equity Release Option

Often Asked Concerns

What Age Do I Required to Be for Equity Release?

The age need for equity Release usually begins at 55 for many strategies. Nevertheless, some providers may provide options for those aged 60 and above, showing varying terms based on private conditions and lending institution policies.

Will Equity Release Affect My Inheritance?

Equity Release can impact inheritance, as the amount obtained plus rate of interest minimizes the estate's value. Heirs may get much less than anticipated, relying on the building's gratitude and the complete financial obligation at the time of passing.

Can I Relocate Home With Equity Release?

The concern of moving home with equity Release occurs frequently. Typically, individuals can transfer their equity Release plan to a new home, but particular terms might use, requiring examination with the lending institution for advice.

Exist Costs Connected With Equity Release Mortgages?

Costs associated with equity Release home loans can consist of plan charges, valuation costs, and legal expenses. In addition, there may be very early repayment fees, which can affect the total expense and monetary navigate to this site effects for the debtor.

Just How Does Equity Release Effect My Tax Scenario?

Equity Release can influence one's tax situation by potentially enhancing gross income, as released funds are thought about funding. It normally does not incur instant tax obligation liabilities, making it crucial to get in touch with a financial advisor for individualized advice.

Verdict

In summary, the selection of equity Release home mortgages readily available today provides property owners aged 55 and over several paths to access their home's worth - equity release mortgages. Whether selecting a lifetime home loan, home reversion strategy, or other alternatives, each option provides distinctive benefits tailored to individual financial needs. Mindful factor to consider and examination with a monetary consultant are necessary to assure the picked equity Release remedy aligns with monetary conditions and individual objectives, inevitably facilitating notified decision-making for a safe and secure economic future. Equity Release mortgages present various options for property owners aged 55 and over. Equity Release home mortgages provide house owners, typically those aged 55 and over, with a way to access the worth tied up in their property without requiring to sell it. Enhanced Lifetime Mortgages use distinct benefits for qualified property owners seeking to Release equity from their residential or commercial properties. Equity Release mortgages, especially in the form of common gratitude home loans, supply property owners an unique economic option that allows them to access funds by leveraging the value of their residential or commercial property. In recap, the selection of equity Release home loans readily available today provides house owners aged 55 and over multiple pathways to access their property's worth

Report this page